Get Paid to Own Beam Communications

A satellite hardware company left for dead, but with a breakeven profitable business, strategic alternatives in review and selling below its cash value.

Beam Communications Holdings Limited (ASX: BCC) is a Melbourne-based satellite hardware original equipment manufacturer (OEM) and telecom service business. At A$0.061 per share the stock trades below its hard cash floor of A$0.066/share meaning the market is pricing the operating business at negative A$0.4 million. This creates an asymmetric entry point: the downside is bounded by cash value, while the upside is a free option on a strategic transaction currently in progress, lead by an aligned management that has a 30% stake of the company.

Beam was recently bought out of a 50/50 Joint Venture called NOLEO following a long and expensive legal process (that has depressed earnings). Their share of the joint venture was bought out for A$13.5M. At the time of settlement they had A$3.5M on the balance sheet. They returned $12M to shareholders in a return of capital on May 1. All together that is an cash value of of A$5.7M Today the market cap is A$5.3M. So this is an operating business you are receiving for free. This also isn’t counting the A$1.3M in tangible book value.

Normalizing Q2 financials (post-JV royalties after the sale, and other errata), the company has an operating cash flow of -$400k annualized, and is targeting $700k in cost savings by the end of the year, so let’s call this breakeven. Consider that it makes $10M in revenue, and $4M in gross profit, it could be attractive for an acquirer if taken private or sold for parts.

There are 86.42M shares out, and insiders own ~20M, so they are incentivized to maximize value for shareholders. They are also actively unlocking value for shareholders. With the following statements released recently:

“Beam is also undertaking a strategic review of its business and is currently reviewing proposals put forward by various parties.” - 27 February 2026

“[We] have completed an initial review of a range of strategic opportunities and are now progressing a focused subset of initiatives, with an emphasis on those most likely to deliver shareholder value. These initiatives remain at an early stage and subject to ongoing evaluation.” - April 23, 2026

So we have a free business, undergoing a strategic review. Now let’s consider, what is the operating business and how much is it worth? More than negative $400,000? I think so.

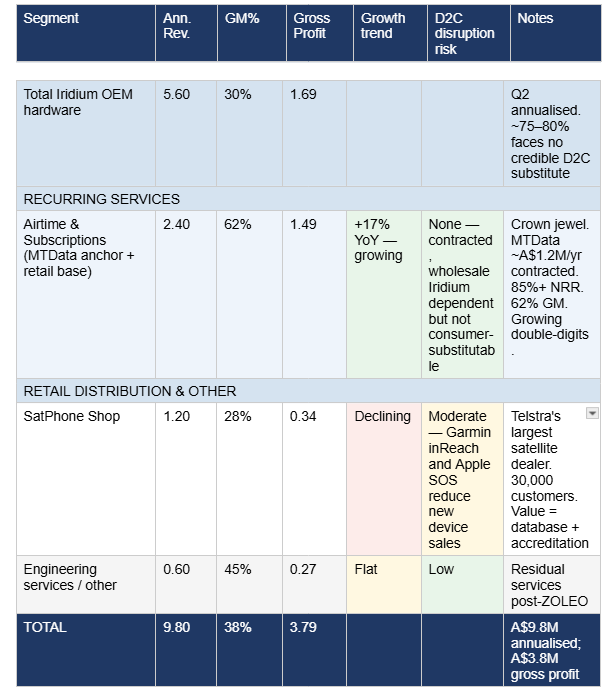

Beam Communications Holdings Limited (ASX: BCC) designs, develops, and manufactures satellite hardware and distributes satellite airtime services. The business comprises three segments: Iridium OEM hardware manufacturing, SatPhone Shop retail, and Airtime & Subscriptions.

Iridium OEM Hardware Manufacturing

Beam is the exclusive original equipment manufacturer of the Iridium GO!/exec: a portable Certus 100 satellite WiFi hotspot that connects up to four devices simultaneously and supports two concurrent voice lines. Beam was selected as OEM partner for both the original Iridium GO! (launched 2014, 67,500+ units shipped) and the Iridium GO!/exec (launched February 2023).

The GO!/exec is a premium device (retail US$1,200–1,800) designed for professionals and enterprises requiring reliable global satellite connectivity. It provides multi-device WiFi hotspot capability, standalone speakerphone, ethernet port, 88 Kbps download speed, IP65 weatherproofing, MIL-STD-810H military-grade ruggedness, and 24/7 SOS via IERCC. Critically, it is classified as a land mobile device running on Iridium Certus 100 midband not a maritime broadband terminal.

The Iridium OEM contract had a minimum commitment of US$12 million over five years from mid-2022 to mid-2027, with an earliest possible fulfillment date in FY24. Subsequent orders are discretionary. The contract was fufilled EOY 2025.

SatPhone Shop

SatPhone Shop Pty Ltd, a wholly owned subsidiary, operates as Australia’s largest Telstra satellite dealer and an online retailer of satellite phones, plans, and accessories. Revenue was A$0.64 million for H1 FY26 (annualised: approximately A$1.2 million). Gross margins are approximately 28%. The principal value of SatPhone Shop is the Telstra dealer accreditation and the approximately 30,000-customer database.

Airtime & Subscriptions

Beam resells satellite airtime from Iridium and other carriers to end customers, including through the MTData enterprise telematics platform (the anchor customer, representing approximately A$1.2 million of annual contracted recurring revenue) and through SatPhone Shop’s retail base. Airtime revenue was A$1.15 million for H1 FY26, growing +16.7% year-on-year. Gross margin on airtime is approximately 62%, reflecting minimal cost of goods. Beam buys wholesale satellite capacity at contracted rates and resells at retail rates.

This segment is contracted, recurring, growing, high-margin, and has a 85%+ net revenue retention. The MTData relationship is embedded in enterprise fleet telematics infrastructure, making it highly sticky. The Telstra dealer relationship provides ongoing consumer and SME airtime sales.

The approximately 30,000 customers Beam has described as SatPhone Shop’s customer base represent the installed base of activated plan customers, mostly on Telstra plans. The revenue Beam recognises as “SatPhone Shop” airtime or services is the aggregate of dealer commissions and direct plan resale activity, not the gross value of Telstra Mobile Satellite plans in force. The accreditation and the customer database are the real assets.

The practical deterrent is switching cost and relationship depth. Beam has supplied MTData’s satellite hardware and airtime for over 10 years. The integration between Beam’s SBD provisioning, MTData’s hardware platform, and the activation/billing infrastructure is deeply embedded. Switching airtime providers requires re-provisioning every active SIM, updating billing systems, potentially requalifying hardware, and managing service continuity for enterprise customers like Linfox with 5,000+ trucks. That is a significant operational undertaking for perhaps A$50-100K of annual savings not an attractive trade for a Telstra subsidiary.

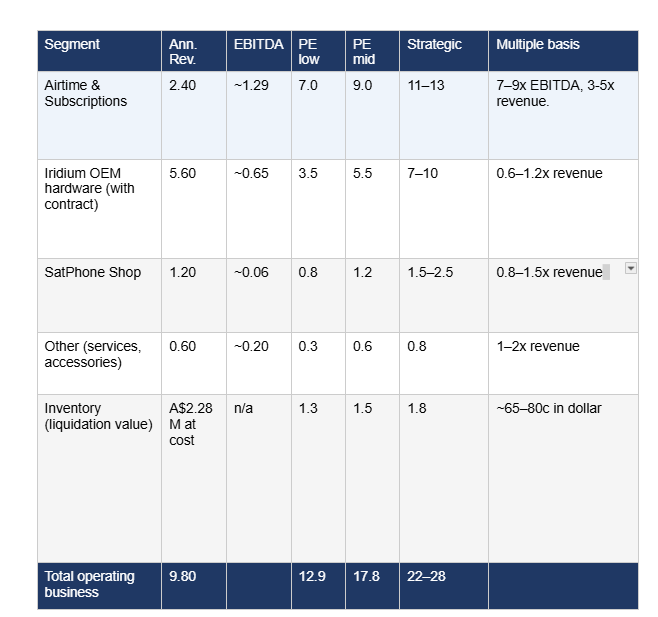

Sum of the Parts Analysis of Each Segment

Competitors to Beam’s GO!/exec are in different product categories.

Beam’s primary product the GO!/exec at US$1,200–1,800 is a portable satellite WiFi hotspot that provides voice calls, data connectivity for multiple users, laptop connectivity, ethernet port, and standalone speakerphone. ZOLEO for example sells at US$149–200 and is a recreational messaging device that pairs with your phone via Bluetooth to send texts.

Competitors like ZOLEO, SOS support, Amazon and Starlink products have no voice call support, no data and no app support. They have no global coverage (only iridium offers this today) these are devices only for messaging, tracking, SOS. So it appears that there is no serious enterprise competition expected until 2030. They serve fundamentally different purposes at fundamentally different price points.

Notably the company has previously navigated competition well. Apple SOS and ZOLEO launched in 2022 and Iridum still signed a deal with Beam in 2023.

Valuation

These segments are contractually fragile but practically more durable than I think most expect. Using a SOTP analysis, we can estimate the value of the remaining operating segments.

Likely Acquirers of the Company

The most probable near-term bidder is Pivotel, which I give a 35% likelihood of acquisition. As Australia’s fourth-largest mobile carrier with six prior acquisitions under its belt and an existing relationship as a Beam reseller, Pivotel is well-positioned to acquire the Telstra dealer channel. What it values most is the airtime book combined with the Telstra dealer relationship and the SatPhone customer database. The strategic synergy lies in cross-selling Pivotel plans to the 30,000 existing customers. As an operational synergy buyer in the private equity range, a likely offer would fall between A$0.20 and A$0.26 per share.

For season Group, led by Carl Hung, I give a a 20% probability. Hung serves as CEO of Season Group, which is Beam’s contract manufacturer, and he is also the third-largest shareholder at 6.41%. This gives him perfect operational visibility and makes the deal a natural vertical integration play, combining manufacturing, brand, Iridium OEM intellectual property, and distribution under one roof. However, because this would be a related party transaction, it would require independent board approval and a shareholder vote. Pricing would likely fall between A$0.20 and A$0.26 per share.

For Iridium Communications (IRDM), I give a 20% probability. CEO Matt Desch has been explicitly open to bolt-on acquisitions and has paused buybacks specifically to pursue M&A. Beam is Iridium’s most important OEM partner, making this a defensive acquisition that would prevent a competitor from acquiring the distribution channel. Iridium would value the OEM intellectual property most highly (20-year certifications, firmware, and product development) alongside the Telstra airtime distribution and SatPhone dealer network. As the buyer most likely to pay a full strategic premium for the OEM IP (and with the deepest pockets) Iridium could offer A$0.28 to A$0.37 per share post-distribution. This would be the most value-maximizing scenario for shareholders.

For a private equity or satellite roll-up I give a 15% probability, framed around Asia-Pacific satellite services consolidation. The thesis would be to acquire the airtime book. The floor range would be A$0.18 to A$0.22 per share post-distribution.

Finally, a management buyout led by Stewart carries about a 10% probability and would emerge primarily as a fallback if external bids fail to clear the valuation threshold. Stewart holds 12.6% of shares and could potentially bring Hung in as a co-investor. Like the Season Group scenario, this would require independent board approval and a shareholder vote. The strategy would be to run the business for cash, maximize airtime growth, and delist to eliminate the A$0.3 million annual listing costs. Pricing would likely come in at or slightly above liquidation value ($0.06/share), raising minority squeeze concerns and making this the least value-maximizing outcome for shareholders.

Important Note: This may be classified as a PFIC (Passive Foreign Investment Company) and all the tax implications that entails. Do your own research and speak with a tax specialist. I own this in an IRA.

Conclusion

In conclusion, Beam’s operating busines sells for a less than $0, but has breakeven in profitability, and that will not face major competition for at least 3 years. The market is writing off the operating business entirely. Meanwhile insiders with significant skin in the game are working working on selling the company to multiple credible bidders in their active strategic review.

Risks are that cash burn increases before significant startegic alternatives close and that a definitive Iridium contract non-renewal announcement destroys the OEM valuation before such a time.

Disclaimer: The information provided in this publication is for informational and educational purposes only and should not be construed as investment advice, financial advice, or a recommendation to buy or sell any securities. I am not a licensed financial advisor, and the views expressed are solely my own. Any investment decisions you make are at your own risk. Always do your own due diligence or consult a licensed financial advisor before making any financial decisions. Past performance is not indicative of future results.

I do hold a position in these securities.

Trading below cash with insiders holding 30% is exactly the setup that makes illiquid micro-caps worth the digging.

The real leverage isn't the discount — it's whether the strategic review timeline closes before the market finds a reason to re-price that optionality away.

Every "free operating business" stays free until someone decides it isn't.

Can you explain how you got to the cash figure?

This is my thinking:

Latest confirmed release says $16.4 million (31 March 2026, pre-return)

$16.36M − $12.1M = ~$4.26M (this assumes zero operating activity in between, which isn't realistic)

Cashflow

H1 FY26 (Jul–Dec 2025)+$2.47M

Q3 FY26 (Jan–Mar 2026)+$64K

Beam itself guided that Q4 revenue would "hold around current levels"

So for Q4 FY26 (Apr–Jun 2026), reasonable expectation: roughly breakeven to modestly positive. Call it $0 to $300K.

That brings us to around ~4.3M to ~4.6M