Portfolio Positions May 2026

Portfolio performance has been good YTD: 22% vs the SNP's 5%. Uncorrelated to the market.

Portfolio Sells This Quarter:

Hoyne Bancorp Inc (HYNE) on 3/2/26 with a 1% return.

I wrote this up on VIC in December, but I sold this position after speaking with folks at Gator Capital and other bank analysts I respect. They need to see a better record of operating performance before investing in this regardless of the strong cash position today.

It sells at 0.72x book, is breakeven profitable now but is growing it loan book well. If you are into small community banks keep an eye on this one.

Lycos Energy Inc (LXCEF) on 3/20/26 with a 115% return.

It hit my price target of 1.20, and the announced merger of Mahikan Oil seemed to have been priced in. It was an oil field in Canada selling for 33% of peers.

MTY Food Group Inc (MTYFF) on 4/9/26 with a -6% return.

The strategic review has taken longer than I anticipated, perhaps due to poor consumer spending recently. I increased my time frame which was reduced by expected return and dropped this position below my hurdle rate.

CVD Equipment Corporation (CVV) on 4/30/26 with a 64% return.

Sold after hitting my price target. CVV Equipment was selling for a market cap of $28M ($4 a share) but had $23M in cash on the balance sheet for a profitable and now streamlined core business. It was almost free so I bought it. That very strong downside protection made this a no-brainer. When it reached its fair value I sold. A big thanks to Hughie Forbes for that one!

I think it fairly valued here, but I read an interesting write up on MicroCapClub suggesting that there is additional upside optionality in terms of future contracts. There is something there, but I am less optimistic than the author on that.

Medical Facilities Corp (MFCSF) on 5/5/2026 with a 7% return.

I sold this after revisiting the thesis and revaluing the company lower than I originally had.

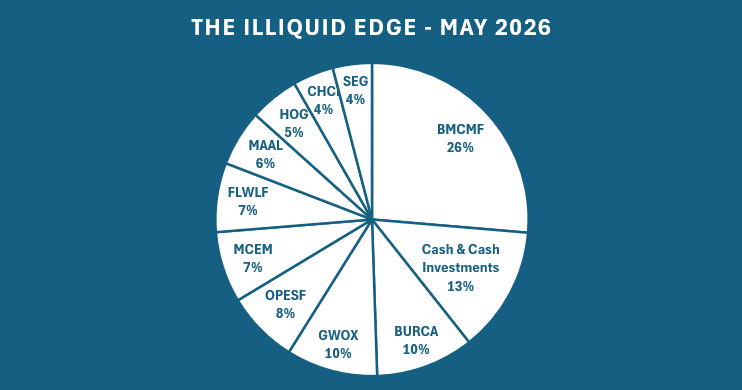

Current Positions:

NEW: Beam Communications Holdings Ltd (BMCMF)

Type: Free Company, Special Situation, Insider Ownership, Roadkill (?)

Daily Average Volume: $20,000

I recently covered Beam in a recent post. The market cap is less than the cash on the balance sheet so is essentially a free company. Insiders own 30%. It is undergoing a strategic review. I expect the strategic review to conclude by the end of the year. My price target is around A$0.25. It trades for A$0.06. The market has left it for dead and values the enterprise at $0. It’s worth more than that.

Burnham Holdings Inc (BURCA)

Type: Cheap Growth

Daily Average Volume: $25,000

Also covered in my previous write up. 10% FCF yield. Earnings are depressed due to an investment in expanding their manufacturing footprint. This is an ideal time to buy before earnings inflect.

Goodheart-Willcox Company Inc (GWOX)

Type: Special Situation, Growth

Daily Average Volume: $19,000

Covered in my previous write up. A growing company selling at a 12% FCF to market cap yield. I expect a corporate event within the year. More information will be gleaned from their annual report which comes out in July.

Otello Corporation ASA (OPESF)

Daily Average Volume: $160,000

Type: Growth, Discount to NAV, Buybacks

Also covered in my previous write up. It is trading at a 38% discount to NAV, has been growing at 17% a year and the company has been buying back 10% of its stock each year.

Monarch Cement Co (MCEM)

Type: Growth

Daily Average Volume: $142,000

Also covered in my previous write up. Cement is a solid “gravel pit” type business that has strong geographic barriers to competition. A durable business that will not be made obsolete any time soon. And comes with a skilled capital allocator at the helm that can compound book value at 16% a year.

NEW: Fleetwood ltd. (FLWLF)

Type: Cheap Earnings, Turnaround, Good co-Bad co.

Daily Average Volume: $500,000

This is a new position. EBIT of 38M. Market Cap of 150M. 30M net cash and significant land assets. That is a 26% earnings yield with a significant cash buffer and very strong downside protection. Fleetwood generates $40M in EBIT a year through its owned workforce accommodation village in Karratha, Western Australia (good co). This is an area where housing supply is significantly constrained. It also owns 2 roughly breakeven segments that Management appears to be open to selling. A new CEO makes shareholder friendly actions more likely.

The Marketing Alliance, Inc (MAAL)

Type: Cheap Earnings, Buybacks

Daily Average Volume: $13,000

Also covered in my previous write up. It trades at a 10% earnings yield with 30% of its market cap in cash. And an expected 10% a year deployed into share buybacks.

NEW: Harley-Davidson Inc (HOG)

Type: Cheap Earnings, Turnaround, Cyclical, Insider Buys, Stock Repurchases

Daily Average Volume: $95,000,000

This is a new position and not very illiquid at all (sorry), but it is so cheap I had to buy some. When you deconsolidate the non-recourse financing from the core operating business, you are buying the core operating business for 1.4B (I bought at 700M), which earns around 400M in mid-cycle EBITDA (management targets 350M by 2027) This is effectively a 25% earnings yield.

New management is taking significant actions to turnaround the operating business by introducing entry level bikes, returning the brand to its roots and resetting relationships with dealers. It has a very strong asset floor with liquidation value of $19.25/share making this an asymmetric bet.

Comstock Holding Companies Inc (CHCI)

Type: Cheap Compounder

Covered in my previous write up. While the stock price appreciated and I trimmed, it is still below my price target. I expect it to compound at 20% a year over the next 5 years.

NEW: Seaport Entertainment Group Inc (SEG)

Type: Low P/B, Turnaround, Insider Ownership

Daily Average Volume: $1,800,000

Seaport Entertainment is a small cap special situation trading at $25/share versus a liquidation value of $35-65/share. It owns real estate assets in short supply: Pier 17 and seaport district in lower Manhattan, a Triple A baseball franchise, a Las Vegas ballpark, an 80% interest in certain Las Vegas air rights, a stake in Jean-Georges Restaurants.

Using a sum of the parts liquidation calculation, I value the assets if sold at $36 at a minimum. New management has successfully taken action to turnaround the troubled properties in New York that have depressed earnings and valuations. Management recognises the significant undervaluation of the stock and have been buying back shares.

Cash

Unfortunately the Beam Communications deal included a dividend distribution that I will not receive for a few weeks and so this is effectively a cash balance I am forced to carry right now.

Beam: I think the value case does not hold anymore. The latest reporting as per June 30, 2026, shows Beam ended the quarter with just 4.0M cash - roughly 0.047 /share, so the downside cushion has shrunk materially. Operating cashflow was a reported outflow of 168K for the quarter.

Nice write up, I like a lot of the names. I also own Fleetwood, unfortunetly for me I paid around the $2.50 AUD mark per share and have been nursing my losses. My initial thesis was the likely strong performance of the community solutions business unit (remote workforce accodomation in Western Aus) which ultimately eventuated and as you mentioned generates the majority of the groups earnings -- however I did not have the foresight on the exceptional underperformance H1 FY26 of the building solultions business unit which wiped a lot of the cash generation of the business for that half - much to my ignorance.

I am a bit apprehensive about the building solutions/construction segment for the remainder of FY 26 - Aus (like a lot of other countries) is under supply chain and inflationary pressures especially in construction -- what's your opinion on this BU moving forward and do you have a different view? It's just such a low margin unit, and im of the opinion that are just so many areas when opex and capex increases can wipe earnings, even an offset from the village accomodation BU doesn't seem to be appreciated by the market.

Lachie

Sydney, Australia